RESERVE BANK OF INDIA AND FOREIGN EXCHANGE MANAGEMENT ACT, 1999.

1.RESERVE BANK OF INDIA – ROLE AND FUNCTIONS:

- RBI was established on April 1, 1935 with a responsibility, inter-alia, of maintaining internal / external value of Indian currency, in accordance with the provisions of the RBI Act 1934. Reserve Bank of India was nationalised in the year 1949.

- The major functions of RBI are:

Bank of Issue, Banker to Government, Bankers’ Bank and Lender of the Last Resort, Controller of Credit Custodian of Foreign Reserves, Supervisory functions, Promotional functions. - As a part of these functions, Reserve Bank of India exercised controls relating to internal/external value of INR through instructions issued to the public and the authorised dealers in foreign exchange and bullion in the form of circulars, public notices, etc. The directions in which control was required were a matter for decision by Government, but the Reserve Bank’s advisory role was an important one; a great deal of initiative in this matter lay with the Bank.

- The first move towards devising a system of exchange control for the sterling area was made in April 1939. Thus Exchange control was introduced as a temporary measure in 1939.

- The initial instructions issued by the Bank in respect of exchange control as well as those issued from time to time modifying, deleting or adding to them were codified and published in the form of an Exchange Control Manual in June 1940; revised editions of the Manual were issued from time to time.

- Foreign Exchange Regulation Act was passed in March 1947 (FERA 1947).

- The Foreign Exchange Regulation Act (FERA) was legislation passed in 1973 and came into force with effect from January 1, 1974. FERA imposed stringent regulations on certain kinds of payments, the dealings in foreign exchange and securities and the transactions which had an indirect impact on the foreign exchange and the import and export of currency. The bill was formulated with the aim of regulating payments and foreign exchange. Comprehensive amendments were made to FERA, especially with respect to foreign investment, to add strength to the liberalisations announced in the economic policies.

- FERA 1973 was replaced by FEMA 1999. The Indian government formulated the Foreign Exchange Management Act (FEMA) in 1999 and was effective from 1st June, 2000. Its main objective was to facilitate external trade and payment and promote the orderly development and maintenance of foreign exchange market in India. This act introduced more liberal provisions in keeping with the requirements of liberalised regimes. Eight decades of Foreign Exchange can be divided in to three phases

- Controls

- Regulations

- Reforms

2.OBJECTIVES:

FEMA was introduced by the Finance Minister in Lok Sabha on August 4, 1998. The Bill aimed “to consolidate and amend the law relating to foreign exchange with the objective of facilitating external trade and payments and for promoting the orderly development and maintenance of foreign exchange market India.” It was adopted by the parliament in 1999 and is known as the Foreign Exchange Management Act, 1999. This Act extends to the whole of India and shall also apply to all branches, offices and agencies outside India owned or by a person resident in India. FEMA was enacted to consolidate and amend the law relating to foreign exchange with the objective of facilitating external trade and payments and for promoting the orderly development and maintenance of foreign exchange market in India. The statement of objects and reasons set the tone of the enactment of new legislation. Some of the highlights of the FEMA 1999 are:

- FERA, 1973 was in existence up to 31.05.2000. FEMA, 1999 came into effect from 01.06.2000.

- FEMA 1999 consolidate the law relating to foreign exchange with the objective of facilitating external trade and payments and for promoting the orderly development and maintenance of foreign exchange market in India.

- There was a Shift in objective from control / conservation to facilitation.

- Government and RBI’s powers were more clearly towards achievement of the above mentioned objectives.

- No arrest. Prosecution to prove charges against accused. A new concept – Compounding was introduced.

- Absence of Mens Rea. Sun-set clause introduced.

- It extends to whole of India and shall also apply to all branches, offices and agencies outside India owned or controlled by a person resident in India and also to any contravention there under committed outside India by any person to whom this Act applies.

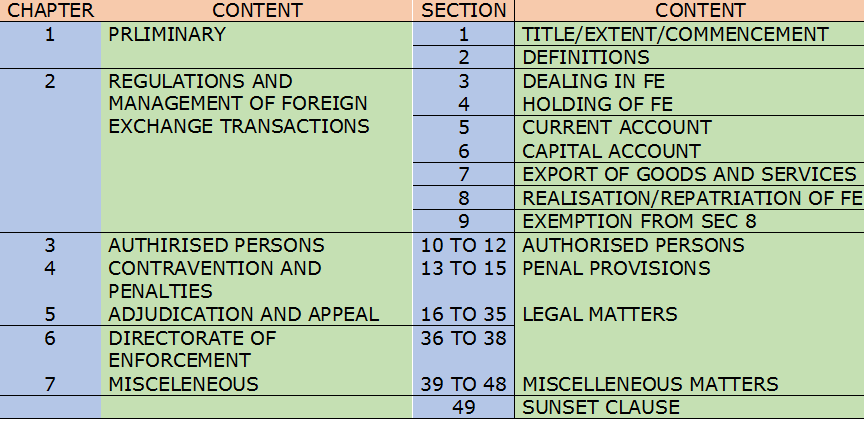

3.IMPORTANT SECTIONS:

There are 49 sections under FEMA 1999 divided in to seven chapters. Important amongst them are as under:

Gist of some of the important sections is as under:

Section 2 – Definitions:

“Person resident in India” means-

(i) a person residing in India for more than one hundred and eighty-two days during the course of the preceding financial year but does not include-

(A) a person who has gone out of India or who stays outside India, in either case-

(a) for or on taking up employment outside India, or

(b) for carrying on outside India a business or vocation outside India, or

(c) for any other purpose, in such circumstances as would indicate his intention to stay outside

India for an uncertain period;

(B) a person who has come to or stays in India, in either case, otherwise than-

(a) for or on taking up employment in India, or

(b) for carrying on in India a business or vocation in India,

or

(c) for any other purpose, in such circumstances as would indicate his intention to stay in India for an uncertain period;

(ii) any person or body corporate registered or incorporated in India,

(iii) an office, branch or agency in India owned or controlled by a person resident outside India,

(iv) an office, branch or agency outside India owned or controlled by a person resident in India;

“Person resident outside India” means a person who is not resident in India;

Section 4 – Holding of foreign exchange, etc.– No person resident in India shall acquire, hold, own, possess or transfer any foreign exchange, foreign security or any immovable property situated outside India.

Section 5 – Current account transactions.– Any person may sell or draw foreign exchange to or from an authorized person if such sale or drawl is a current account transaction: Provided that the Central Government may, in public interest and in consultation with the Reserve Bank, impose such reasonable restrictions for current account transactions as may be prescribed.

Section 8 – Realization and repatriation of foreign exchange.- Where any amount of foreign exchange is due or has accrued to any person resident in India, such person shall take all reasonable steps to realize and repatriate to India such foreign exchange within such period and in such manner as may be specified by the Reserve Bank.

Section 9 – Exemption from realization and repatriation in certain cases.- The provisions of sections 4 and 8 shall not apply to the following, namely:-

(a) possession of foreign currency or foreign coins by any person up to such limit as the Reserve Bank may specify;

(b) foreign currency account held or operated by such person or class of persons and the limit up to which the Reserve Bank may specify;

(c) foreign exchange acquired or received before the 8th day of July, 1947 or any income arising or accruing thereon which is held outside India by any person in pursuance of a general or special permission granted by the Reserve Bank;

(d) foreign exchange held by a person resident in India up to such limit as the Reserve Bank may specify, if such foreign exchange was acquired by way of gift or inheritance from a person referred to in clause (c), including any income arising there from;

(e) foreign exchange acquired from employment, business, trade, vocation, services, honorarium, gifts, inheritance or any other legitimate means up to such limit as the Reserve Bank may specify; and

(f) such other receipts in foreign exchange as the Reserve Bank may specify.

Section 10 – Authorised person. – The Reserve Bank may, on an application made to it in this behalf, authorize any person to be known as authorized person to deal in foreign exchange or in foreign securities, as an authorized dealer, money changer or off-shore banking unit or in any other manner as it deems fit. An authorization under this section shall be in writing and shall be subject to stipulated conditions.

Section 13. Penalties.- If any person contravenes any provision of this Act, or contravenes any rule, regulation, notification, direction or order issued in exercise of the powers under this Act, or contravenes any condition subject to which an authorization is issued by the Reserve Bank, he shall, upon adjudication, be liable to a penalty up to thrice the sum involved in such contravention where such amount is quantifiable, or up to two lakh rupees where the amount is not quantifiable, and where such contravention is a continuing one, further penalty which may extend to five thousand rupees for every day after the first day during which the contravention continues.

4.HOW IMPLEMENTED?:

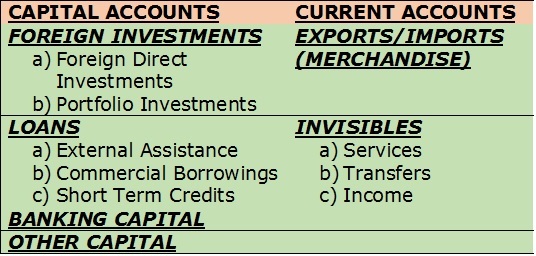

The Foreign Exchange Transactions can broadly be divided in to two types of transactions to which FEMA 1999 is applicable:

- Current Account Transactions

- Capital account transactions

Article 2 under FEMA 1999 defines the term ‘Current Account Transaction’ as a transaction other than a capital account transaction and without prejudice to the generality of the foregoing such transaction includes,

(i) Payments due in connection with foreign trade, other current business, services, and short-term banking and credit facilities in the ordinary course of business,

(ii) Payments due as interest on loans and as net income from investments,

(iii) Remittances for living expenses of parents, spouse and children residing abroad, and

(iv) Expenses in connection with foreign travel, education and medical care of parents, spouse and children;

In the above definition, the words “without prejudice to the generality of the foregoing such transaction includes” imply that even if the transactions listed above may fit into the definition of capital account transactions, such transactions shall be treated as current account transactions. For example, resident of India imports goods from outside India on a short term credit (for a period of less than 6 months), he is creating a liability outside India and thus, it can be treated as a capital account transaction but, it is specifically included in the above definition as a current account transaction.

As a general rule, any person may sell or draw foreign exchange if such sale or drawal is a current account transaction. Under the Act, Central Government may, in public interest and in consultation with the Reserve Bank, impose such reasonable restrictions for current account transactions as may be prescribed. Accordingly, the Central Government has issued the Foreign Exchange Management (Current Account Transaction) Rules, 2000. It contains the list of current account transactions for which drawal of foreign exchange is:-

- Totally prohibited (Schedule I)

- Permitted, subject to the prior approval of concerned Ministry, Central Government (Schedule II);

- Permitted, subject to the transaction is within the prescribed limit (Schedule III) ;

- No restrictions or limits are applicable for undertaking the transactions that are not covered by the above rules and the authorized dealers are free to release foreign exchange upon the satisfaction that the transactions will not involve and is not designed for the purpose of, violation of the Act, or any rules, regulations made there under.

In view of the above we may consider, Indian rupee as fully convertible so far as current account transactions are concerned except the restrictions as above. This implies that foreign exchange is freely available to the residents for remittance on account of current account transactions for the various purposes like foreign travel, foreign education, and medical treatment abroad etc. The non residents are also freely allowed to remit outside India the income or capital gain generated in India. However, the Indian rupee, in respect of capital account transactions, is not fully convertible.

“Capital Account Transaction” is defined as a transaction which alters the assets or liabilities, including contingent liabilities, outside India of a persons resident in India or assets or liabilities in India of persons resident outside India, and includes transactions referred to in sub-section (3) of section 6 of the Act.

Alters the assets and liabilities, outside India, of a person resident in India. For example:- (i) a resident of India acquires an immovable property outside India or acquires shares of a foreign company. This way his/her overseas assets are increased; or (ii) a resident of India borrows from a non-resident through External commercial Borrowings (ECBs). This way he/she has created a liability outside India.

Alters the assets or liabilities in India of persons resident outside the India. In other words, it includes those transactions which are undertaken by a non-resident such that his/her assets or liabilities in India are altered (either increased or decreased). For example, (i) a non-resident acquires immovable property in India or acquires shares of an Indian company or invest in a Wholly Owned Subsidiary or a Joint Venture with a resident of India. This way his/her assets in India are increased; or (ii) a non-resident borrows from Indian housing finance institute for acquiring a house in India. This way he/she has created a liability in India.

The Act has empowered the Reserve Bank of India (RBI) to specify, in consultation with the Central Government, the permissible capital account transactions and the limits upto which foreign exchange may be drawn for these such transactions. But it shall not impose any restriction on the drawal of foreign exchange for payments due on account of amortization of loans or for depreciation of direct investments in the ordinary course of business. Accordingly, the RBI has issued notifications governing capital account transaction. The FEMA Notification No. 1/2000 dated 3-5-2000 contains the list of permissible capital account transactions as well as list of prohibited capital account transactions.

- The permitted capital account transactions have been classified into two categories:-

- Capital account transactions by persons resident in India includes,

- Investment in foreign securities;

- Foreign currency loans raised in India and abroad;

- Acquisition and transfer of immovable property outside India;

- Guarantees issued in favour of a person resident outside India;

- Export, import and holding of currency or currency notes;

- Loans and overdrafts (borrowings) from a person resident outside India;

- Maintenance of foreign currency accounts in India and outside India;

- Taking out the insurance policy from an insurance company outside India;

- Remittance outside India of capital assets of a person resident in India;

- Sale and purchase of foreign exchange derivatives in India and abroad and commodity derivatives abroad.

- Capital account transactions by non- residents includes,

- Investment in India such as (i) issue of security by a body corporate or an entity in India and investment therein by a non-resident and (ii) investment by way of contribution to the capital of a firm or a proprietary concern or an association of persons in India;

- Acquisition and transfer of immovable property in India;

- Guarantee in favour of, or on behalf of, a person resident in India;

- Import and export of currency/currency notes into/from India;

- Deposits between a person resident in India and a person resident outside India;

- Foreign currency accounts in India of a non-resident;

- Remittance of the assets in India held by a non-resident.

There are generally two types of prohibitions on capital account transactions :-

General Prohibition:- A person shall not undertake or sell or draw foreign exchange to or from an authorised person for any capital account transaction. This prohibition is subjected to the conditions specified by Reserve Bank in its circulars and notifications.

Special Prohibition:- A non resident person shall not make investment in India in any form, in any company or partnership firm or proprietary concern or any entity, whether incorporated or not, which is engaged or proposes to engage:- (i) in the business of chit fund, or (ii) as Nidhi Company, or (iii) in agricultural or plantation activities or (iv) in real estate business, or construction of farm houses or (v) in trading in Transferable Development Rights (TDRs).

5.BALANCE OF PAYMENT:

The balance of payments is a statistical statement that systematically summarizes, for a specific time period, the economic transactions of an economy with the rest of the world. Transactions, for the most part between residents and nonresidents, consist of those involving goods, services, and income; those involving financial claims on, and liabilities to, the rest of the world; and those (such as gifts) classified as transfers. A transaction itself is defined as an economic flow that reflects the creation, transformation, exchange, transfer, or extinction of economic value and involves changes in ownership of goods and/or financial assets, the provision of services, or the provision of labor and capital.

The majority of these items can be broadly categorised under head Capital Account transaction and Current Account transaction summarised in the chart.

To understand this, Please visit India’s latest Balance of Payment:

6.FOREIGN EXCHANGE RESERVES:

Strictly foreign exchange reserve is the total of a country’s foreign currency deposits and bonds held by the central bank and monetary authorities. However, the term often refers to the total of a country’s gold holdings, convertible foreign currencies held in its banks, plus special drawing rights (SDR) and exchange reserve balances with the International Monetary Fund (IMF).

In the past, during the Bretton Woods system — an international monetary system formed after the second

World war, foreign exchange reserves were used by countries through their central banks to maintain the external value of their currencies at fixed rate. Subsequently, with the collapse of this system, the focus changed. Reserves are now generally maintained by countries for meeting their international payment obligations — both short and long terms, including sovereign and commercial debts, financing of imports, for intervention in the foreign currency markets during periods of volatility, besides helping to boost the confidence of the market in the ability of a country to meet its external obligations and to absorb any unforeseen external shocks, contingencies or unexpected capital movements.

India’s foreign exchange reserves comprise foreign currency assets, gold and special drawing rights allocated to it by the International Monetary Fund (IMF) in addition to the reserves it has parked with the fund.

Foreign exchange reserves are held and managed by the RBI. Some countries use external managers to handle their reserves. The composition of the reserves is not disclosed to the public.

However, the foreign currency assets are invested mainly in instruments abroad which have the highest credit rating and which do not pose any credit risk.

These include sovereign bonds, treasury bills and short-term deposits in top-rated global banks besides cash accounts. The country’s central bank is also reckoned to have invested in top-rated bonds of entities like Fannie Mae in the US.

Earlier, the adequacy of reserves was measured by the level of such reserves in relation to imports. In other words, the amount of reserves which a country had to cover imports for say three to six months or so was considered as an measure of adequacy.

However, with the change in the patterns of global trade and other developments including several currency crises, the adequacy is measured against benchmarks like not only import cover, but also percentage of reserves to short-term debt, as a proportion of external debt, ratio of reserves to GDP besides as a ratio to broad money and reserve money and size of the current account deficit and possible variations in capital flows into the country.

Reserve Bank of India is declaring the position of Foreign Exchange Reserves every Friday.

Please go through the latest position of Foreign Exchange Reserves here:

7.FACILITIES UNDER FEMA 1999:

FERA 1973 was replaced by FEMA 1999. The Government formulated the Foreign Exchange Management Act (FEMA) in 1999 and was effective from 1st June, 2000. Its main objective was to facilitate external trade and payment and promote the orderly development and maintenance of foreign exchange market in India. This act introduced more liberal provisions in keeping with the requirements of liberalized regimes.

As stated earlier, the objective of FEMA was to facilitate the Foreign Exchange Transactions in India and not to restrict as was the case in earlier regime.

The Foreign Exchange Transactions can broadly be divided in to two types of transactions to which FEMA 1999 is applicable:

- Current Account Transactions

- Capital account transactions

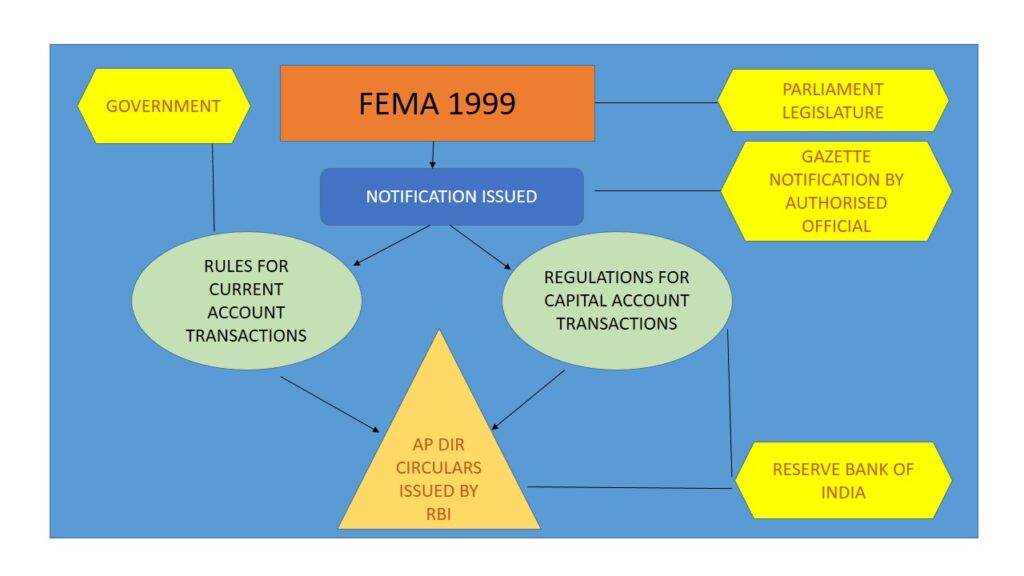

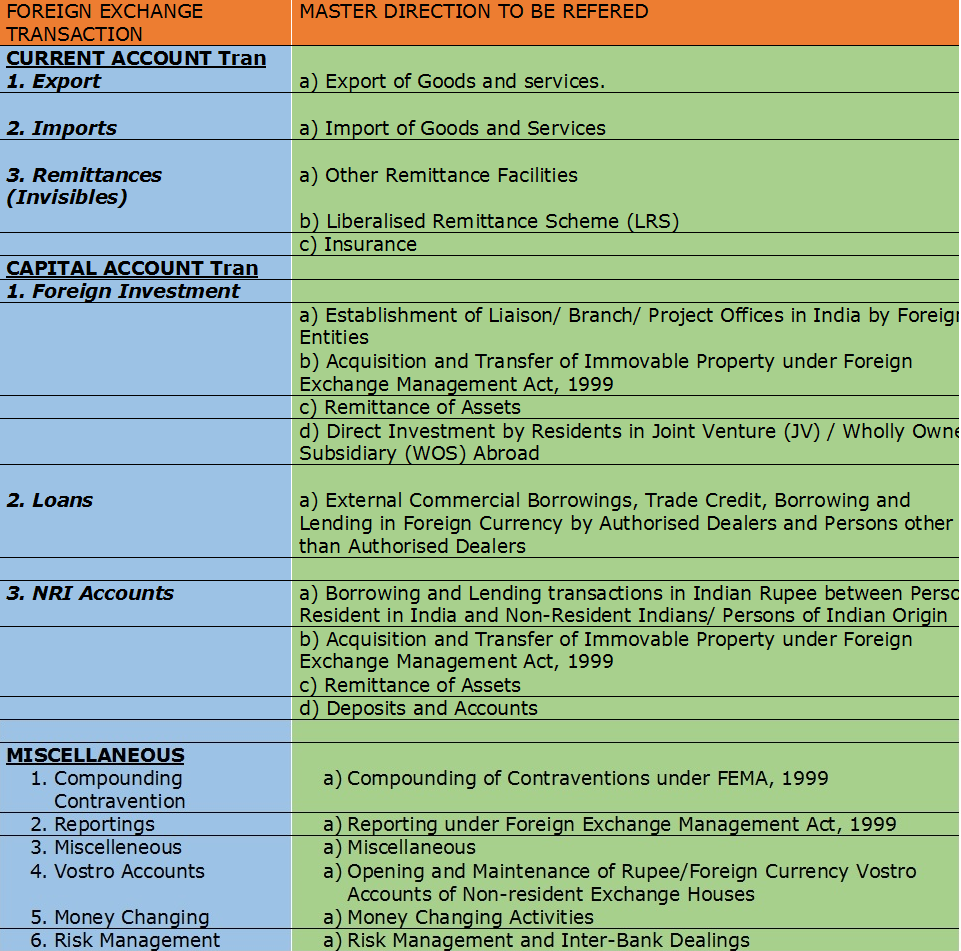

We have broadly classified these transactions in to various areas as mentioned in the following paragraph. Reserve Bank is issuing Master Directions, consolidating prevailing guidelines, relating to these areas. Throughout the year, RBI issues AP DIR Circulars to update these guidelines. Master Directions are simultaneously updated. One need to refer to the Master Directions to have guidelines on the subject. These guidelines give the details of the facilities available in various areas relating to Foreign Exchange, to Residents and Non-Residents.

The table below will enable you to refer to the relevant Master Directions relating to the guidelines on the subject. The details of these guidelines are given subject-wise, in this website under the respective headings.

8AUTHORISED PERSONS UNDER FEMA 1999:

RBI cannot do all transactions in foreign exchange by itself. Therefore, the powers are delegated to authorised persons with suitable guidelines, to deal in foreign exchange and foreign securities.

Sec. 3 of FEMA 199 require all Dealing in FE through Authorised Persons only.

Sec 2 (c) of FEMA 1999 define Authorised Persons means an Authorised Dealer, Money Changer , Offshore Banking Unit or any other person authorised u/s 10 (1) to deal in Foreign Exchange or Foreign Securities.

Under Sec 10 (1) of FEMA 1999 empowers RBI to authorise person to deal in Foreign Exchange or Foreign Securities.

Authorised Paersons can be broadly categorized in the following categories:

- AUTHORISED DEALERS:

- Category I

- Category II

- Category III

- Full Fledged Money Changers (FFMC):

- Off shore Banking Units (OBU):

Authorised Dealers:

List of AD Banks Category wise is available on RBI website under Notifications ->FEMA ->ADs list

Category-I of the list contains all major Banks in India who are providing all Current Account and Capital account Transactions.

Category-II of the list contains upgraded FFMCs, State Co-Operative Banks, urban Co-Operative Banks, RRBs and others who are authorized to deal in non-trade Current Account Transactions.

Category-III of the list contains selected financial and other Institutions, who are authorized to deal with specific transactions incidental to their Foreign Exchange Activities.

Full Fledged Money Changers (FFMCs):

These are the institutes who facilitate purchase and sale of Foreign Exchange for private or business visit. Detailed guidelines relating to their activities are given in RBI Master Circular on Money Changing Activities.

Off shore Banking Units (OBU):

These are the Banking units, usually established in a specialized area like SEZ where the transactions are entertained in foreign currency only.

9.PENAL PROVISIONS UNDER FEMA 1999

CONTRAVENTION AND PENALTIES

If any person contravenes any provision of the Act, or contravenes any rule, regulation, notification, direction or order issued in exercise of the powers under the Act, or contravenes any condition subject to which an authorizations issued by the Reserve Bank, he shall, upon adjudication, be liable to a penalty up to thrice the sum involved in such contravention where such amount is quantifiable, or up to two lakh rupees where the amount is not quantifiable, and where such contravention is a continuing one, further penalty which may extend to five thousand rupees for every day after the first day during which the contravention continues.

Any Adjudicating Authority adjudging any contravention, may, if he thinks fit in addition to any penalty which he may impose for such contravention direct that any currency, security or any other money or property in respect of which the contravention has taken place shall be confiscated to the Central Government and further direct that the foreign exchange holdings, if any, of the persons committing the contraventions or any part thereof, shall be brought back into India or shall be retained outside India in accordance with the directions made in this behalf.

For the purposes of this sub-section, “property” in respect of which contravention has taken place, shall include-

(a) deposits in a bank, where the said property is converted into such deposits;

(b) Indian currency, where the said property is converted into that currency; and

(c) any other property which has resulted out of the conversion of that property.

Enforcement of the orders of Adjudicating Authority.– If any person fails to make full payment of the penalty imposed on him within a period of ninety days from the date on which the notice for payment of such penalty is served on him, he shall be liable to civil imprisonment.

Power to compound contravention.-(1) Any contravention may, on an application made by the person committing such contravention, be compounded (Compounding refers to the process of voluntarily admitting the contravention, pleading guilty and seeking redressal) within one hundred and eighty days from the date of receipt of application by the Director of Enforcement or such other officers of the Directorate of Enforcement and officers of the Reserve Bank as may be authorized in this behalf by the Central Government in such manner as may be prescribed.

(2) Where a contravention has been compounded , no proceeding or further proceeding, as the case may be, shall be initiated or continued, as the case may be, against the committing such contravention under that section, in respect of the contravention so compounded.

DIRECTORATE OF ENFORCEMENT

(1) The Central Government shall establish a Directorate of Enforcement with a Director and such other officers or class of officers as it thinks fit, who shall be called officers of Enforcement, for the purposes of this Act.

(2) The Central Government may authorise the Director of Enforcement or an Additional Director of Enforcement or a Special Director of Enforcement or a Deputy Director of Enforcement to appoint officers of Enforcement below the rank of an Assistant Director of Enforcement.

(3) Subject to such conditions and limitations as the Central Government may impose, an officer of

Enforcement may exercise the powers and discharge the duties conferred or imposed on him under this Act.

Power of search, seizure, etc. – (1) The Director of Enforcement and other officers of Enforcement, not below the rank of an Assistant Director shall take up for investigation the contravention.

(2) The Central Government may also, by notification, authorise any officer or class of officers in the Central Government, State Government or the Reserve Bank, not below the rank of an Under Secretary to the Government of India to investigate any contravention.

(3)The officers shall exercise the like powers which are conferred on income-tax authorities under the Income-tax Act, 1961 and shall exercise such powers, subject to such limitations laid down under that Act.

EMPOWERING OTHER OFFICERS

(1) The Central Government may, by order and subject to such conditions and limitations as it thinks fit to impose, authorise any officer of customs or any central excise officer or any police officer or any other officer of the Central Government or a State Government to exercise such of the powers and discharge such of the duties of the Director of Enforcement or any other officer of Enforcement under this Act as may be stated in the order. (2).The officers shall exercise the like powers which are conferred on the income-tax authorities under the Income-tax Act, 1961, subject to such conditions and limitations as the Central Government may impose.

10. MISCELLANEOUS MATTERS:

Presumption as to documents in certain cases:

In legal proceedings under FEMA, documents are tendered as evidence.

Any such document-

(i) May be produced or furnished by any person or may have been seized from the custody of control of any person under laws; or

(ii) May have been received from any place outside India in the course of investigation of any contravention under this Act alleged to have been committed by any person.

Suspension of operation of this Act

(1) If the Central Government is satisfied that circumstances have arisen rendering it necessary that any permission granted or restriction imposed by this Act should cease to be granted or imposed, or if it considers necessary or expedient so to do in public interest, the Central Government may by notification, suspend or relax to such extent either indefinitely or for such period as may be notified, the operation of all or any of the provisions of this Act.

(2) Where the operation of any provision of this Act has under sub-section (1) been suspended or relaxed indefinitely, such suspension or relaxation may, at any time while this Act remains in force, be removed by the Central Government by notification.

(3) Every notification issued under this section shall be laid, as soon as may be after it is issued, before each House of Parliament, while it is in session, for a total period of thirty days which may be comprised in one session or in two or more successive sessions, and if, before the expiry of the session immediately following the session or the successive sessions aforesaid, both Houses agree in making any modification in the notification or both Houses agree that the notification shoul not be issued, the notification shall thereafter have effect only in such modified form or be of no effect, as the case may be; so, however, that any such modification or annulment shall be without prejudice to the validity of anything previously done under that notification.

Power of Central Government to give directions

For the purposes of this Act, the Central Government may, from time to time, give to the Reserve Bank such general or special directions as it thinks fit .The Reserve Bank shall, in the discharge of its functions under this Act, comply with any such directions.

Contravention by companies

A person committing contravention of any of the provisions of this Act or any rule, direction or order made there under may be a company. In such case, every person who, at the contravention was committed, was in charge of, and was responsible to the company for the conduct of the business of the company as well as the company, shall be deemed to be guilty of the contravention took place without his knowledge or that he exercised due to diligence to prevent such contravention.

Bar of legal proceedings

No suit, prosecution or other legal proceeding shall lie against the central Government or the Reserve Bank or any officer of the Central Government or of the Reserve Bank or any other person exercising any power or discharging any functions or performing any duties under this Act for anything in good faith done or intended to be done under this act or any rule, regulation, notification, direction or order made thereunder.

Rules and regulations to be laid before Parliament

Every Rule and Regulation made under this Act shall be laid, as soon as may be after, it is made, before each House of Parliament, while it is in session for a total period of 30 days may be comprised in one session or in two or more successive sessions. If both Houses agree in making any modification in the Rule or Regulation, the Rule and Regulation shall have effect only in such modified form. If both Houses agree that Rule or Regulation should not be made, the Rule or Regulation shall thereafter be of no effect. However, any such modification or annulment shall be without prejudice to the validity of anything previously done under that Rule or Regulation.